Restoring The Power Law

Building UK Tech Sovereignty Requires a Venture Capital System Working At Full Capacity.

TL;DR

The UK consistently fails to scale startups into globally dominant tech companies — the power law (a few breakthrough bets returning everything) is what determines national prosperity, but we’re not necessarily optimising for it.

Sovereign AI is a welcome and ambitious initiative — but it enters a sprawling landscape of well-intentioned public financing institutions (e.g. BBB, NWF), and a venture capital ecosystem with structural flaws worth fixing.

The British Business Bank has historically been stuck in the middle of a bifurcated VC market — not backing small/novel emerging funds, nor anchoring truly large growth rounds. This awkward middle is exactly where venture capital no longer works. Though in fairness the BBB is starting to change direction.

Only ~8% of European VC partners are ex-founders vs. 60%+ in Silicon Valley, which is a big problem.

The National Wealth Fund is struggling to absorb its new mandate of investing in critical technology infrastructure, given its historical capability has been energy and green infrastructure.

Across the UK’s public financing bodies, success is measured in inputs not outcomes — companies supported, capital deployed — and no one has defined what a UK “national winner” even means.

Recommendations & Low-Hanging Fruit

Back ex-founders to launch funds, with fast-tracked compliance and CGT rollover relief for founders using sale proceeds to set up their own funds.

Build a BBB-SovAI longitudinal data library to track outcomes and make UK private markets legible to pension capital.

Carve out £5bn of the National Wealth Fund for enabling infrastructure for critical technology, with the technical capacity necessary, to help de-risk deeptech investment.

Set out “national winner” criteria — not a strict definition, but a set of criteria so that we are all speaking broadly on the same page about what success looks like.

Create a Foreign VC Landing scheme to attract top-tier US funds to the UK, reducing the incentive for founders to chase capital abroad.

The Power Law

Back in April, the government launched UK Sovereign AI (SovAI) – a £500 million state-backed fund that will make direct equity investments in AI startups, along with access to compute and other carrots like rapid visa decisions. While it’s always easy to pick holes in government initiatives, it’s also worth stepping back and lauding the fact that there are at least parts of government which are genuinely ambitious – and who understand that one of the core reasons for the UK’s malaise is the fact that we have not built enough globally leading companies in the last several decades. And that this must be a priority.

However, it is worth zooming out and asking whether the overall architecture of UK public involvement in private markets and venture capital (VC) is working, and what its aims actually are (many of the most important arguments in this space have been made by Alex Chalmers already).

SovAI now sits alongside the British Business Bank (BBB), the National Wealth Fund (NWF), and the National Strategic Sovereign Investment Fund (NSSIF) – as well as other initiatives like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) – as government initiatives in the UK’s investment (mainly VC) ecosystem. Though all with varying mandates and capabilities, these institutions broadly stem from the same diagnosis and impetus. Put glibly, the archetypal explanation is:

The UK has no lack of early-stage startups or cutting-edge R&D, but it is consistently unable to scale these companies into the kinds of the large, “anchor” technology firms (of the likes of Meta and Google) which not only produce immediate jobs and tax revenue, but act as a centre of gravity for capital, talent and supply chains. The “market failure” is that there is not sufficient capital and/or risk appetite to invest in these companies – even if the long term returns are worthwhile. Hence there is a place for government intervention.

But the even more fundamental concept driving all of this – and Venture Capital itself – is the “power law” (or at least it should be). This is the idea that, in VC, the majority of investments fail. One or two, if you back the right thing at the right moment, return the fund many times over. In other words, one big bet makes the payoff for all the rest – and could have generationally-defining results for the UK economy.

The point is this: if scaling tech companies is increasingly the determinant of economic prosperity and power, then the health of our venture capital ecosystem (and government’s involvement within it) is also critical to British power and sovereignty. The question is, to what extent are we optimising for and delivering on that goal? And, where we aren’t – and where the UK’s VC ecosystem is perhaps lacking – what are meaningful interventions that could shift the dial?

If Britain’s future depends on the “power law”, then we should check whether we are getting it right.

Some Critiques

Stuck in the Middle With You?

The BBB was established in 2013 to purportedly address a classic problem: the chronic underfunding of innovative UK SMEs at the growth stage. It has grown into the UK’s largest LP in domestic venture funds.

Historically, however, the BBB has spent much its time LP-ing medium sized VC funds – often for multiple rounds. British Patient Capital’s €25 million commitment to Nauta Capital’s fifth fund is the clearest example: the BBB backed the fifth round of a medium-sized fund.

To understand why this is an issue, we need some context of where VC is right now. Global VC has bifurcated. There are mega-funds — capturing the lion’s share of LP capital, making their economics on the management fee — and cottage funds, sub-£100 million vehicles that stay lean, often outperform on IRR, and reach corners of the ecosystem that no large fund would bother with. The mediocre middle is dying. The BBB therefore needs to operate at these extremes: back high-risk emerging funds that might scope genuinely novel deep-tech areas megafunds miss, while also providing cornerstone capital to anchor genuinely large rounds.

But the BBB appears too often to be playing in the middle:

It’s often not going big: For example, looking at British Patient Capital’s direct co-investment portfolio — the arm specifically designed to back growth-stage companies — only 15 of 61 anchored rounds in the past five years were at Series B or above, according to Tracxn data.

It’s not going small: the BBB tends to look for fund managers with track records. That sounds well and good on paper. But, actually, if you want i) More ex-founders setting up their own funds (see below) ii) Smaller deeptech funds that are good at spotting trends or companies that the bigger funds miss iii) A bit more competition in the VC space generally – it’s a good idea to LP new, dynamic fund managers (who may not have a long track record on investing, but have a strong track record of actually building).

The problem with being “stuck in the middle” is that the middle is really not where venture capital works anymore.

This does appear to be changing, however. The BBB is gradually moving towards backing bigger rounds. Most recently, a £40m cornerstone commitment to Eka Ventures and £100m cornerstone to a healthcare fund. It’s new, broader aim is to channel 60% of venture growth investment towards scaleups, writing larger cheques to leading fund managers.

This direction is promising, as if the BBB is to operate effectively it must double down on the extremes.

Mind The Ex-Founder Gap

Here’s a stat I think is essential: more than 60% of Silicon Valley’s most successful funds have former founders or executives as partners. In Europe, that figure is around 8%.If the UK and Europe are to build more competitive VC ecosystems, this gap needs to close.

Having more ex-founders in VC not only means more successful funds, it also means that diamonds in the rough are less likely to be missed: in deep tech (quantum, biotech, robotics) the problem is not just capital availability, but also information asymmetry. Most fund managers do not always know what they are looking at if a credible team pitches them a photonics innovation or new chip design. This isn’t just an issue for the odd startup that goes under the radar and fails to raise, it risks having a systemic impact on the market – where certain areas of the innovation ecosystem are overlooked because there is simply not the technical capacity amongst investors to spot it. You are therefore more likely to end up with a herd mentality, where everyone tacks from software, to AI, to quantum based on what’s hot at a given moment.

However, the UK’s VC ecosystem appears to be structurally unfriendly to new ex-founders entering into VC. First, as discussed, because the BBB generally looks to LP those with track records (which does make sense within a certain logic) – which can entrench incumbent syndicates to the detriment of new entrants.

Second, compliance costs are often prohibitive. A first-time manager raising £10 million must find a compliance officer, run monthly reporting, and commission annual external reviews — requirements designed for institutions managing hundreds of millions. They act as a structural barrier to exactly the small, specialist, ex-founder funds that could most improve information flow in the ecosystem.

Some UK VCs really stand out in getting this right. At Kindred Capital, for example, almost all of their partners are ex-founders. More interestingly, they employ an approach whereby every founder that Kindred backs gets a carry in the fund itself, effectively becoming a co-owner of the fund. This is designed to incentivise an ecosystem where founders have a stake in each other’s success.

If we want to have a more dynamic UK VC ecosystem, we need more ex-founders running funds.

The National Wealth Fund’s Technology Gap

The Invest Strategy 2035 expanded the National Wealth Fund’s mandate, instructing it to deploy its £27.8 billion in funding “more strategically to drive growth” in the UK’s frontier industries — including, for the first time, digital and technologies alongside its traditional energy infrastructure focus. The ambition is right. A £27.8 billion fund with a genuine technology remit could be investing in the critical enabling infrastructure the UK desperately needs: testbeds for inference compute, self-driving labs, advanced semiconductor packaging.

This matters for the VC ecosystem. When speaking to investors looking to back areas like quantum hardware, one thing that comes up often is the fact that they face a double risk — not just on the technology and the company, but also on the infrastructure that often doesn’t exist. A well-functioning NWF is therefore one of the most direct levers available to de-risk private venture investment in deep tech.

The problem is that the NWF is not yet fully equipped to deliver on this. Its predecessor was built around energy infrastructure, and the technology track record reflects that. Currently, therefore, this is a heavily underutilised vehicle sitting on a large pile of capital.

Defining “Winners”

A pattern that links a lot of UK public finance institutions (BBB, NWF etc) is that there are almost no real criteria for measuring success. Often, success is measured in terms of activity rather than outcomes: number of companies supported, capital deployed, funds LP-d. But these are inputs not outputs.

And here is the crux of it: if government involvement in venture capital is intended not to generally support SMEs but to scale true proto-champions – to double down on the power law, and correct the market where it appears to be failing to do so – then without measurement criteria how can we know if this is working? In fact, if what in fact we are doing is measuring the number of companies receiving support (this applies for EIS and SEIS too), then is this not undermining the core principle of the power law: that most should be allowed to fail, and only a few make it?

There is also, perhaps, an even more elemental point which evades definition – and will apply to Sovereign AI. What do we mean by a “national winner”, exactly? Does this mean a UK-listed company, a UK-headquartered company, a company with significant R&D activity in the UK a company that pays most of its tax in the UK? It may be that all or a combination of these matter. Without clarity, people will likely bias towards the most negative definition in any given situation (as has been the case with recent criticism about the Advanced Research Innovation Agency (ARIA) granting £50m to US tech and VC).

For what it’s worth, I personally think that we should not index on stiflingly rigid definitions, or whether the company is listed on the London Stock Exchange. The likes of DeepMind should be seen as success stories because it has anchored leading talent and R&D in London, not as a failure because it is owned by Google.

But if, in the new age of techno-industrial strategy, the government is increasingly playing the game of power laws and backing winners then we do need a conversation about what “winners” are.

Some Solutions

Back Ex-Founders

Back in its early days, Sequoia ran a scheme where it would give a credible ex-founder a $150,000 cheque to start their own small fund. In exchange, they would get to see where the founder was placing their early bets. The logic was to get more people with genuine founder expertise into the investment ecosystem, and to leverage their instincts as a market information signal – shining a lamp onto the more dimly lit parts of the startup pipeline.

The UK should introduce an equivalent: writing modest cheques for strong ex-founders looking to set up their own funds. The eligibility period should not track investor record but founder record, and compliance should be fast-tracked. This could sit with SovAI, or elsewhere. It should also come alongside a Business Assets Rollover Relief (though applied to a VC): whereby founders selling a business would be exempt from Capital Gains Tax if they were using part of the proceeds to create their own fund.

Build a BBB-SovAI Data Library

[This is not an original idea. Andrew Bennett called for something very similar in his Centre for British Progress report on British Sovereign Capital].

The BBB has, over its years, accumulated visibility into hundreds of UK startups across the growth pipeline — funding stages, sectors, geographies, follow-on outcomes. No private LP has anything close to that systemic view. SovAI will add to it.

Together, they could start to build a comprehensive, longitudinal dataset on UK venture capital — which is currently highly opaque.

Not only would this help British public capital track its success properly, by looking at outcomes rather than inputs, it would likely have other positive secondary effects. For example, one of the biggest barriers to UK institutional investors putting money into domestic private markets is opacity (and therefore perceived risk). A credible view of UK venture performance would make the case far more legible than any amount of mandatory arm-twisting – proving to pension managers that there are major returns to be had in British private markets.

A Critical Technology Infrastructure Unit in the NWF

The UK could really do with a National Wealth Fund that had the capacity and capital to invest in the enabling critical technology infrastructure of the future. But investing in a grid upgrade and investing in a national inference compute testbed require fundamentally different capabilities.

The government should therefore establish a dedicated Critical Technology Infrastructure unit within the NWF, ringfenced with around £5 billion in capital and staffed with genuine technical expertise — people who understand what inference compute capacity or a self-driving lab actually requires, and can structure investments accordingly. This is not a new institution; it sits within the NWF’s existing framework and mandate. But it would give critical technology infrastructure a distinct identity, a dedicated investment team, and clear accountability. And it should start by scoping 5-10 critical infrastructures for future technology – including inference compute testbeds, self-driving labs, advanced packaging etc. And the best thing about it is that the capital is already committed, so no Treasury roadblocks ahead…

Ultimately, we want VC to take bets on technologies and companies – not also having to take bets on enabling infrastructure.

Define What a “National Winner” Looks Like

As the impetus to build a trillion-dollar UK company builds, we increasingly need a criteria (though not a rigid definition) of what a UK national winner looks like.

This is because, much of government policy and spending is implicitly designed to back proto-winners without explaining what that means. That includes everything from:

BBB funding rounds.

SovAI investments.

NWF equity investments (though this is mostly infrastructure).

Procurement: now that procurement is increasingly becoming a tool explicitly used for industrial strategy – to help provide demand-signalling to deeptech companies – we need to define what success looks like beyond the immediate access to capabilities that the government is paying for (i.e. how effectively is procurement working as an industrial strategy lever). [I lay some of these problems here in my assessment of the government’s latest quantum procurement programme].

Without a sense of what success is we may end up focusing on the wrong thing. For what it’s worth, I think we tend to over-fixate on where companies list rather than where their operations and R&D bases are.

The government should therefore set out a series of non-strict but descriptive criteria that loosely explain what is meant by a national winner. This might be different for across different companies and industries which have varying characteristics. The point is not that we have strict metrics, but that when we talk about building the UK companies of the future (and spending taxpayer money on scaling them) we are broadly singing from the same hymn sheet.

Incentivise Top-Tier Foreign VC to Setup in the UK

Now this might seem counterintuitive or incite rebukes of: “But we want more sovereign, British capital going into British companies! Not more investment from the US that allows them to pinch our biggest winners”.

I think this is the wrong way of thinking about foreign capital for a few reasons:

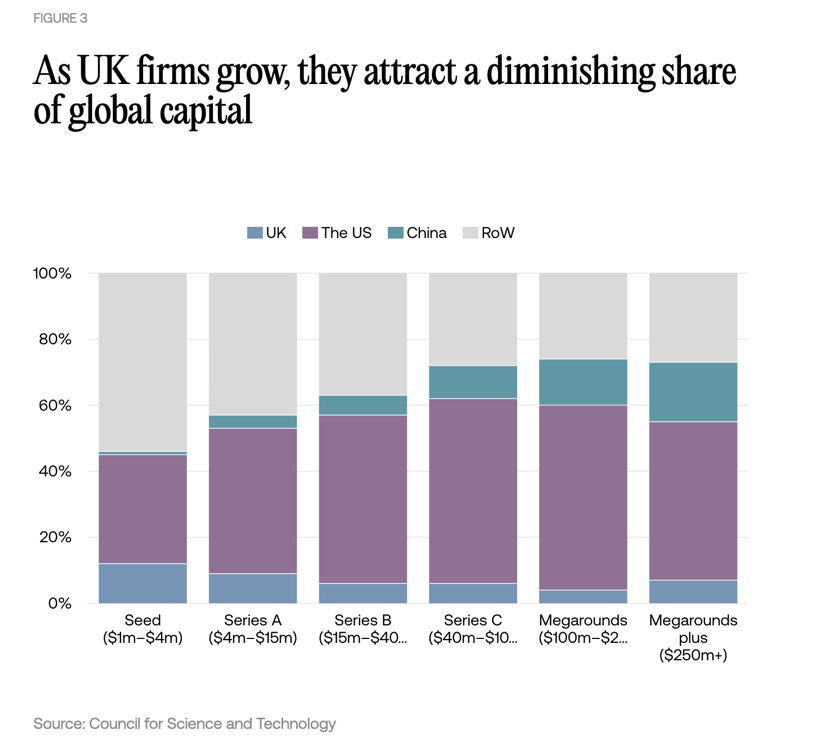

Keep your enemies close: If you think about why it is that people get nervy about U.S. venture capital coming into the UK – it’s because there’s a correlation between the companies that receive more U.S. capital, and those that are more likely to pack up and leave to the U.S. for good to be closer to where the investors are. Indeed the presence of U.S. VC in the UK goes up at each stage of raising (see figure below). But one of the reasons why this happens is that great UK startups have to chase the money -- which is in the U.S. But if more of those U.S. VCs had bases in the UK, top UK founders would have less reason to move to the U.S. to chase the capital.

More capital is generally always good: Currently the approximate model is that UK capital (state and private) goes into early-stage startups, then eventually a U.S. company buys the UK company on the cheap around about Series B. As someone lugubriously put it to me once: “The U.S. don’t actually invest in UK startups, they just poach them on the cheap”. In other words, wouldn’t it be better to have more U.S. investment, rather than more underpriced U.S. buyouts?

More competition: Now we’re getting into really vibe-based speculation. But my instinct is that more top-notch U.S. venture capital would inject a bit more competition and dynamism into the UK’s own VC ecosystem – compelling the best fund managers to really show up and compete for the top startups rather than take a leisurely portfolio approach, rely on BBB LPs or early-stage tax breaks.

The Andreessen Horowitz London episode — where a satellite office opened with considerable fanfare in 2023, quietly wound down — is instructive. We need to do more to make it attractive for top tier foreign venture capital to set up here.

My suggestion would be a Foreign VC Landing scheme: fast-tracked visa decisions, streamlined regulation, expedited FCA authorisation, access to BBB co-investment, for funds above a certain AUM threshold and that commit to having a substantive UK presence and deploying a meaningful share of each new fund into UK companies.

If there is indeed a capital/equity gap in the UK (though this is heavily debated) why not fill it with more foreign private capital, not just public money?

Venture Capital and UK Sovereignty

If we want to build UK national winners that drive productivity, anchor innovation, and give us a stake in a geopolitical world comprised of hard power and frontier tech – then we need to ensure our venture capital ecosystem is operating to its full potential. But in an age of industrial strategy, there is a lot of impetus for state intervention and not always much impetus for stepping back and checking whether we are getting it right. I believe that UK public funding institutions (BBB, NWF, NSSIF, now SovAI) do far more good than they do harm. I also, however, think there are flaws that can be fixed, and some quick wins which we should take.

But if the power law is what will determine national prosperity and power, then we must optimise for it.